BDSwiss App

Download & start trading

Marshall Gittler,

Head of Investment Research at BDSwiss, Fundamental Analyst & Financial Contributor

Marshall Gittler,

Head of Investment Research at BDSwiss, Fundamental Analyst & Financial Contributor

What we were looking at before Omicron came along

What we were looking at before Omicron came along Now however the outlook is much less clear. We don’t know how the new variant will affect the global economy. As Fed Chair Powell said in his recent testimony to Congress:

Now however the outlook is much less clear. We don’t know how the new variant will affect the global economy. As Fed Chair Powell said in his recent testimony to Congress:

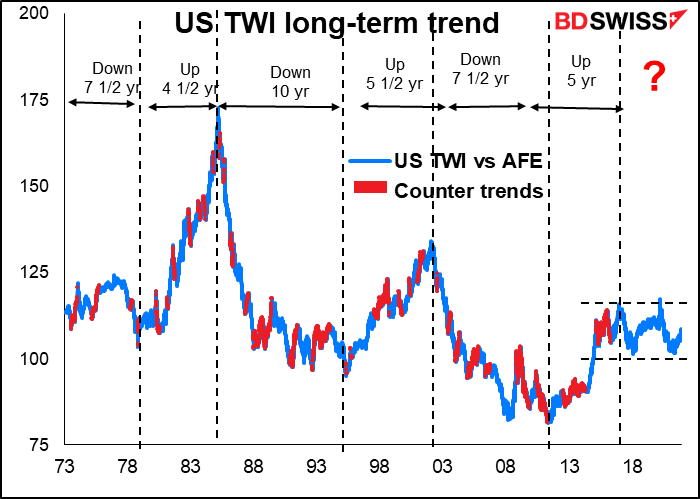

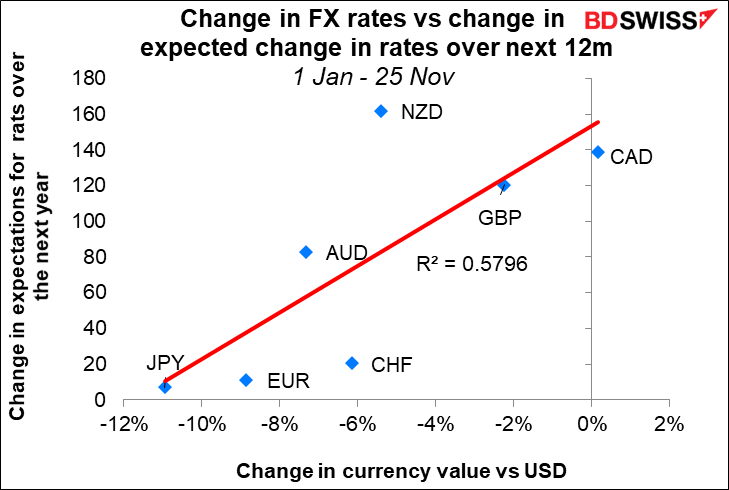

This year, the key for markets has been trying to determine the pace of monetary policy divergence. How quickly are central banks going to start raising rates and how far? Monetary policy convergence went into reverse, and we had the beginning of monetary policy divergence as different central banks were expected to raise rates at different paces. This divergence has been responsible for over half the change in currency rates this year.

This year, the key for markets has been trying to determine the pace of monetary policy divergence. How quickly are central banks going to start raising rates and how far? Monetary policy convergence went into reverse, and we had the beginning of monetary policy divergence as different central banks were expected to raise rates at different paces. This divergence has been responsible for over half the change in currency rates this year. Omicron turns out to be mild

Omicron turns out to be mild That assumption seems to be what’s built into the markets now. Following the discovery of the virus, rate expectations for most countries were revised down (except for Japan, where no one expected it to raise rates anyway). However, they remain positive. People are just assuming a slower, shallower pace of tightening than they were before, but not a wholesale derailment.

That assumption seems to be what’s built into the markets now. Following the discovery of the virus, rate expectations for most countries were revised down (except for Japan, where no one expected it to raise rates anyway). However, they remain positive. People are just assuming a slower, shallower pace of tightening than they were before, but not a wholesale derailment. I’m firmly in the “transitory” camp, even if Fed Chair Powell recently said that the word should be “retired.” Most of the recent increase in inflation is due to the impact of the pandemic. While it may take longer than expected for inflation to get back to more normal levels (hence the idea of retiring “transitory”), I still expect the global economy to gradually adjust to the “new normal” and for inflation to decline next year on its own accord.

I’m firmly in the “transitory” camp, even if Fed Chair Powell recently said that the word should be “retired.” Most of the recent increase in inflation is due to the impact of the pandemic. While it may take longer than expected for inflation to get back to more normal levels (hence the idea of retiring “transitory”), I still expect the global economy to gradually adjust to the “new normal” and for inflation to decline next year on its own accord. As do most forecasters. With the exception of a few countries (the UK, Japan, and China being the main ones), most countries are forecast to have lower inflation in 2022 than in 2021.

As do most forecasters. With the exception of a few countries (the UK, Japan, and China being the main ones), most countries are forecast to have lower inflation in 2022 than in 2021. The starting point: the Fed and the dollar

The starting point: the Fed and the dollar In their quarterly Summary of Economic Projections, the median estimate of the FOMC members put “maximum employment” at around 4.0%, with most estimates ranging between 3.8% to 4.3%.

In their quarterly Summary of Economic Projections, the median estimate of the FOMC members put “maximum employment” at around 4.0%, with most estimates ranging between 3.8% to 4.3%. Some people argue that the Fed is likely to be patient and delay hiking rates until the labor market gets back to where it was before the pandemic, i.e.., an unemployment rate of 3.5% and participation rate of 63.3. However, I think they’re more likely to accept that the structure of the US labor market has changed and a return to those levels is unlikely any time soon, particularly the participation rate as there has been a fundamental change in people’s desire to work. As a result, I think they’ll be OK starting “lift-off” with the unemployment rate approaching what they see as the longer-run level.

Some people argue that the Fed is likely to be patient and delay hiking rates until the labor market gets back to where it was before the pandemic, i.e.., an unemployment rate of 3.5% and participation rate of 63.3. However, I think they’re more likely to accept that the structure of the US labor market has changed and a return to those levels is unlikely any time soon, particularly the participation rate as there has been a fundamental change in people’s desire to work. As a result, I think they’ll be OK starting “lift-off” with the unemployment rate approaching what they see as the longer-run level. Outlook for the dollar: a game of two halves

Outlook for the dollar: a game of two halves There’s another possibility though that results in the same conclusion, just a steeper path up for the dollar in the first half of the year and perhaps a steeper decline later. That is, the Fed could choose to tighten earlier and faster than expected. In his testimony to Congress, Powell said, “The economy is very strong and inflationary pressures are high. It is therefore appropriate in my view to consider wrapping up the taper of our asset purchases… perhaps a few months sooner.” That would mean the dollar would be likely to rise in the early part of the year, probably more than I would anticipate, but then fall back in the second half as other central banks caught up to the Fed.

There’s another possibility though that results in the same conclusion, just a steeper path up for the dollar in the first half of the year and perhaps a steeper decline later. That is, the Fed could choose to tighten earlier and faster than expected. In his testimony to Congress, Powell said, “The economy is very strong and inflationary pressures are high. It is therefore appropriate in my view to consider wrapping up the taper of our asset purchases… perhaps a few months sooner.” That would mean the dollar would be likely to rise in the early part of the year, probably more than I would anticipate, but then fall back in the second half as other central banks caught up to the Fed. At the same time, the capital inflows that have helped the US to finance that may slow. The dollar has been buoyed recently by large inflows into US capital markets, particularly as the US stock market has outperformed other markets globally, but with US valuations high relative to other countries and many of the tech leaders that were driving the rally threatened by the new global rules on corporate taxation, the US market may prove less attractive next year.

At the same time, the capital inflows that have helped the US to finance that may slow. The dollar has been buoyed recently by large inflows into US capital markets, particularly as the US stock market has outperformed other markets globally, but with US valuations high relative to other countries and many of the tech leaders that were driving the rally threatened by the new global rules on corporate taxation, the US market may prove less attractive next year. There is also the risk that the virus could hit the US harder than other countries. See below for more details on that.

There is also the risk that the virus could hit the US harder than other countries. See below for more details on that. Let’s take the currencies one by one. For each, we’ll start out with the market consensus forecast from Bloomberg, which includes both the high and the low estimates for each pair. Bear in mind please that the high and low may reflect the view of just one forecaster, whereas the median is around where most forecasters are located. Nonetheless, the extremes do give you an idea of where the risks are and what the potential moves could be.

Let’s take the currencies one by one. For each, we’ll start out with the market consensus forecast from Bloomberg, which includes both the high and the low estimates for each pair. Bear in mind please that the high and low may reflect the view of just one forecaster, whereas the median is around where most forecasters are located. Nonetheless, the extremes do give you an idea of where the risks are and what the potential moves could be. The market is apparently assuming that the European Central Bank moves to tighten rates and that that gradually pushes up the EUR.

The market is apparently assuming that the European Central Bank moves to tighten rates and that that gradually pushes up the EUR. 2) The US has a habit of tightening faster than the ECB does. If we compare the latest tightening cycle in the US and Europe, the US moved much more rapidly. (We’ll ignore the abortive April 2011 tightening cycle in Europe, which only lasted seven months before they realized it was a dreadful mistake.)

2) The US has a habit of tightening faster than the ECB does. If we compare the latest tightening cycle in the US and Europe, the US moved much more rapidly. (We’ll ignore the abortive April 2011 tightening cycle in Europe, which only lasted seven months before they realized it was a dreadful mistake.) 3) The virus situation is currently much worse in Europe than it is in the US. That may delay tapering and tightening in the EU as more European countries go into lockdown and growth slows.

3) The virus situation is currently much worse in Europe than it is in the US. That may delay tapering and tightening in the EU as more European countries go into lockdown and growth slows. The virus issue could turn around to be a negative for the US, however. The US is in a singularly bad position to fight a new, more virulent strain, for two reasons. First off, the response isn’t national but rather is done on a state-by-state basis. Around half the states are controlled by Republican nutcases who believe it is their patriotic duty to ensure that their citizens are free to die of COVID-19 if they so wish. Secondly, the country has the lowest vaccination rates among the developed nations, which ensures that they will have the chance to do so. This is a major risk for the US and the USD in Q1 of next year.

The virus issue could turn around to be a negative for the US, however. The US is in a singularly bad position to fight a new, more virulent strain, for two reasons. First off, the response isn’t national but rather is done on a state-by-state basis. Around half the states are controlled by Republican nutcases who believe it is their patriotic duty to ensure that their citizens are free to die of COVID-19 if they so wish. Secondly, the country has the lowest vaccination rates among the developed nations, which ensures that they will have the chance to do so. This is a major risk for the US and the USD in Q1 of next year. JPY: return of the yen carry trade?

JPY: return of the yen carry trade? The market consensus is for a weaker yen this year, and I would agree. If anything, I think the currency is likely to weaken more than the market consensus. However please remember that I have a daughter in university in Japan and so I’m naturally biased to hope for a weaker yen, so I may not be an entirely objective observer.

The market consensus is for a weaker yen this year, and I would agree. If anything, I think the currency is likely to weaken more than the market consensus. However please remember that I have a daughter in university in Japan and so I’m naturally biased to hope for a weaker yen, so I may not be an entirely objective observer. That’s probably because the country is expected to still be well below its 2% inflation target two years from now.

That’s probably because the country is expected to still be well below its 2% inflation target two years from now. Eventually, the BoJ may have to adjust or even lift its “yield curve control” program, which keeps the yield on the benchmark 10-year Japanese Government bond at ±25 bps around zero. However, this meeting probably isn’t the time even as other central banks move to normalize policy. Deputy Gov. Amamiya Wednesday made a speech, Japan’s Economy and Monetary Policy, in which he said:

Eventually, the BoJ may have to adjust or even lift its “yield curve control” program, which keeps the yield on the benchmark 10-year Japanese Government bond at ±25 bps around zero. However, this meeting probably isn’t the time even as other central banks move to normalize policy. Deputy Gov. Amamiya Wednesday made a speech, Japan’s Economy and Monetary Policy, in which he said: In short, I think the BoJ is likely to remain on hold while other central banks raise rates and watch their bond markets respond accordingly. The widening yield differential between Japan and other nations is likely to act as a magnet drawing funds out of Japan and weakening the currency.

In short, I think the BoJ is likely to remain on hold while other central banks raise rates and watch their bond markets respond accordingly. The widening yield differential between Japan and other nations is likely to act as a magnet drawing funds out of Japan and weakening the currency. The main question though is, will the authorities change their view on the currency? Up to now the Ministry of Finance was focused on encouraging exports and had a bias for a weaker currency. Now that the country has a trade deficit though perhaps they’re more concerned with ensuring affordable imports and wouldn’t want to see the yen weaken too much further. Verbal intervention by the authorities could limit the downside for the yen (or upside for USD/JPY, to be more precise).

The main question though is, will the authorities change their view on the currency? Up to now the Ministry of Finance was focused on encouraging exports and had a bias for a weaker currency. Now that the country has a trade deficit though perhaps they’re more concerned with ensuring affordable imports and wouldn’t want to see the yen weaken too much further. Verbal intervention by the authorities could limit the downside for the yen (or upside for USD/JPY, to be more precise). One other factor limiting the yen’s downside is positioning. The yen has been speculators’ #1short for several months now. It was only replaced recently by AUD. There might not be that many more people left to get in the trade.

One other factor limiting the yen’s downside is positioning. The yen has been speculators’ #1short for several months now. It was only replaced recently by AUD. There might not be that many more people left to get in the trade. Risk to the forecast: It’s possible that as the global inflation rate rises, Japan’s could, too. Japan’s corporate goods price index, known elsewhere in the world as the producer price index, has been soaring recently. It hit 9.0% YoY in November, the fastest pace of growth since 1980. The final goods PPI rose at the fastest pace since 1981.

Risk to the forecast: It’s possible that as the global inflation rate rises, Japan’s could, too. Japan’s corporate goods price index, known elsewhere in the world as the producer price index, has been soaring recently. It hit 9.0% YoY in November, the fastest pace of growth since 1980. The final goods PPI rose at the fastest pace since 1981. The rise is being driven by higher raw material prices, which are really soaring – up 74.6% YoY!!! That’s the highest rate of growth since the oil shock days of 1974. Intermediate materials were up 15.7% YoY.

The rise is being driven by higher raw material prices, which are really soaring – up 74.6% YoY!!! That’s the highest rate of growth since the oil shock days of 1974. Intermediate materials were up 15.7% YoY. If companies grow tired of absorbing these higher producer prices in their margins, we could see inflation coming back to Japan after a nearly 30-year absence. That would cause a sea change for the Japanese economy and monetary policy – and the yen.

If companies grow tired of absorbing these higher producer prices in their margins, we could see inflation coming back to Japan after a nearly 30-year absence. That would cause a sea change for the Japanese economy and monetary policy – and the yen.

I have to admit: I hate the pound. I think that by all rights it should be at parity with the euro – hell, parity with the Italian Lira if it still existed, or maybe the Greek Drachma (OK, that’s a bit excessive; there’d be some 301 GDR to the dollar right now if it were still around). But still, the currency seems to me to be like Wiley E. Coyote in the “Road Runner” cartoons, running off the cliff and still running until he looks down…

I have to admit: I hate the pound. I think that by all rights it should be at parity with the euro – hell, parity with the Italian Lira if it still existed, or maybe the Greek Drachma (OK, that’s a bit excessive; there’d be some 301 GDR to the dollar right now if it were still around). But still, the currency seems to me to be like Wiley E. Coyote in the “Road Runner” cartoons, running off the cliff and still running until he looks down… The forces all seem arrayed against the pound:

The forces all seem arrayed against the pound: The UK and EU still haven’t worked out the details of their trade agreement for services, but already Brexit has resulted in an estimated 5.7% decline in service exports, according to a recent paper on Brexit and Services Trade. The paper also observed that “Given liberalising services trade is generally more challenging than goods, it is extremely hard, if indeed possible at all, to expect future FTAs (free trade agreements) to achieve new market access in a significant way. After all, gravity dictates that services trade is typically greatest with nearest trading partners.”

The UK and EU still haven’t worked out the details of their trade agreement for services, but already Brexit has resulted in an estimated 5.7% decline in service exports, according to a recent paper on Brexit and Services Trade. The paper also observed that “Given liberalising services trade is generally more challenging than goods, it is extremely hard, if indeed possible at all, to expect future FTAs (free trade agreements) to achieve new market access in a significant way. After all, gravity dictates that services trade is typically greatest with nearest trading partners.” As for portfolio investment, much of that is equities.

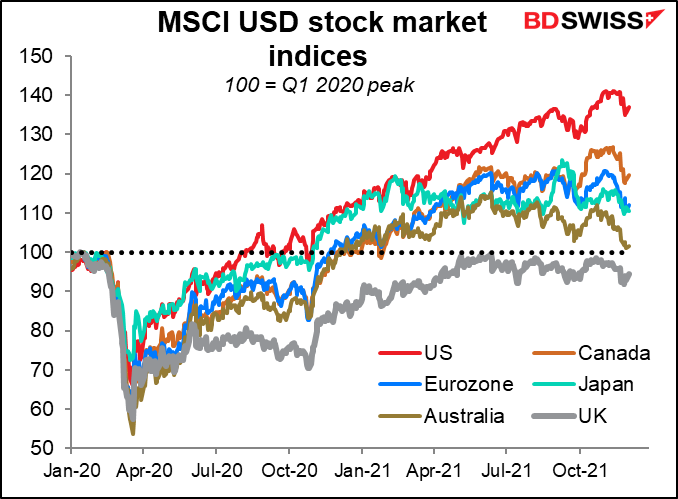

As for portfolio investment, much of that is equities. The UK is the only major world stock market that hasn’t regained its pre-pandemic peak yet in USD terms. (That’s not just because of currency valuation – the FTSE 100 index of major shares hasn’t regained the peak in local currency terms, although the FTSE 250 index of mostly local companies has.)

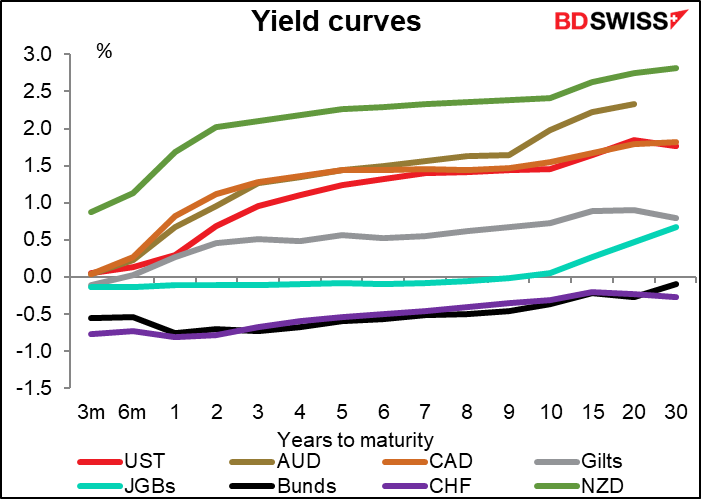

The UK is the only major world stock market that hasn’t regained its pre-pandemic peak yet in USD terms. (That’s not just because of currency valuation – the FTSE 100 index of major shares hasn’t regained the peak in local currency terms, although the FTSE 250 index of mostly local companies has.) That leaves higher gilts yields to attract money in. Given that UK yields are now toward the bottom of the pack in the G10, that would require a substantial rise in interest rates – a rise that the Bank of England would probably not want to see in these fragile times. Accordingly, I expect the pound to take the strain and adjust downward until UK assets become more attractive to international investors.

That leaves higher gilts yields to attract money in. Given that UK yields are now toward the bottom of the pack in the G10, that would require a substantial rise in interest rates – a rise that the Bank of England would probably not want to see in these fragile times. Accordingly, I expect the pound to take the strain and adjust downward until UK assets become more attractive to international investors. The main argument I can see against this one is that the pound has suffered so much already, any further problems are already in the price. Not necessarily! The currency’s real effective exchange rate is only about average nowadays. A further 10% downside on this measure would be nothing extraordinary.

The main argument I can see against this one is that the pound has suffered so much already, any further problems are already in the price. Not necessarily! The currency’s real effective exchange rate is only about average nowadays. A further 10% downside on this measure would be nothing extraordinary. Moreover, Brexit has caused the UK economy to shrink. Estimates are that even before the UK left the EU, the economy was 1%-3% smaller because of foregone consumption and investment (as well as the depreciation of sterling). The government estimates that the economy will be 4%-5% smaller by 2030. Slower growth means a slower increase in productivity and less incentive for foreign investment – all negatives for the currency.

Moreover, Brexit has caused the UK economy to shrink. Estimates are that even before the UK left the EU, the economy was 1%-3% smaller because of foregone consumption and investment (as well as the depreciation of sterling). The government estimates that the economy will be 4%-5% smaller by 2030. Slower growth means a slower increase in productivity and less incentive for foreign investment – all negatives for the currency.

Does it make sense to deal with the three commodity currencies together? I think so. The correlations between them are at fairly high levels historically, especially AUD & CAD. This suggests that the market is lumping them all together to a great degree.

Does it make sense to deal with the three commodity currencies together? I think so. The correlations between them are at fairly high levels historically, especially AUD & CAD. This suggests that the market is lumping them all together to a great degree. Much of their fate will be determined by what happens in China. The recent loosening of monetary policy there, including two cuts in the Required Reserve Ratio (RRR) for banks, is a good sign for future growth in China – and therefore the global manufacturing cycle.

Much of their fate will be determined by what happens in China. The recent loosening of monetary policy there, including two cuts in the Required Reserve Ratio (RRR) for banks, is a good sign for future growth in China – and therefore the global manufacturing cycle. That should also help to underpin global metal prices, which are a major factor in determining AUD’s value.

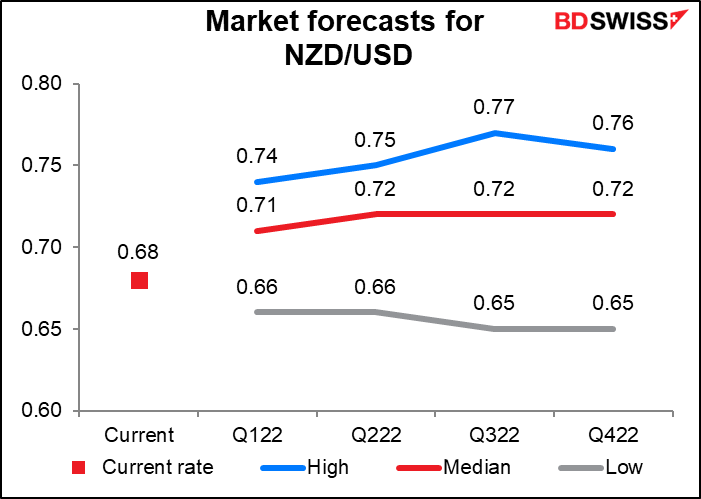

That should also help to underpin global metal prices, which are a major factor in determining AUD’s value. Given that 62% of New Zealand’s exports are edibles, one might assume that global agricultural prices would be much more important for NZD than metal prices, but one would be wrong (except for milk). My research shows that the currency is more correlated with commodity prices overall and with energy prices –even though New Zealand doesn’t export any oil or coal – than with agricultural commodities. My guess is that the FX market isn’t so discerning and that traders just think “commodities” without necessarily thinking which commodities.

Given that 62% of New Zealand’s exports are edibles, one might assume that global agricultural prices would be much more important for NZD than metal prices, but one would be wrong (except for milk). My research shows that the currency is more correlated with commodity prices overall and with energy prices –even though New Zealand doesn’t export any oil or coal – than with agricultural commodities. My guess is that the FX market isn’t so discerning and that traders just think “commodities” without necessarily thinking which commodities. Of course, this reliance on China can cut both ways. Monetary and fiscal stimulus is getting less effective in producing growth in China, thanks to the miracle of diminishing marginal returns. With the real estate sector in serious trouble in the country, growth in China could also be in more trouble than the government can contain simply by monetary meddling.

Of course, this reliance on China can cut both ways. Monetary and fiscal stimulus is getting less effective in producing growth in China, thanks to the miracle of diminishing marginal returns. With the real estate sector in serious trouble in the country, growth in China could also be in more trouble than the government can contain simply by monetary meddling. A recent paper (Peak China Housing, by Harvard Prof. Kenneth Rogoff and IMF economist Yuanchen Yang), estimated that “in 2016, real estate and construction industries combined accounted for around 29% of China’s GDP, comparable only by pre-crisis Spain and Ireland…Real estate not only accounts for 23% of household consumption, but it also connects to various sectors of the economy through investment, construction, and the financial system.” The two economists estimate that “a 20% fall in real estate activity could lead to a 5-10% fall in GDP, even without amplification from a banking crisis, or accounting for the importance of real estate as collateral.” This leaves AUD and NZD vulnerable to a downturn in Chinese construction which, if Evergrande is any indication, seems possible if not likely.

A recent paper (Peak China Housing, by Harvard Prof. Kenneth Rogoff and IMF economist Yuanchen Yang), estimated that “in 2016, real estate and construction industries combined accounted for around 29% of China’s GDP, comparable only by pre-crisis Spain and Ireland…Real estate not only accounts for 23% of household consumption, but it also connects to various sectors of the economy through investment, construction, and the financial system.” The two economists estimate that “a 20% fall in real estate activity could lead to a 5-10% fall in GDP, even without amplification from a banking crisis, or accounting for the importance of real estate as collateral.” This leaves AUD and NZD vulnerable to a downturn in Chinese construction which, if Evergrande is any indication, seems possible if not likely. CAD: watch out for oil

While CAD is classified among the commodity currencies, its fate is tied up closely with one commodity in particular: oil. There’s a very close correlation between USD/CAD and the Bank of Canada’s energy price index (comprised of the prices of coal, oil, and natural gas).

CAD: watch out for oil

While CAD is classified among the commodity currencies, its fate is tied up closely with one commodity in particular: oil. There’s a very close correlation between USD/CAD and the Bank of Canada’s energy price index (comprised of the prices of coal, oil, and natural gas). The oil industry seems to agree that oil is likely to fall next year, as supply increases faster than demand (see below). If that happens, I would expect CAD to decline somewhat. It’s been the best-performing of the three commodity currencies this year, indeed the best-performing of all the G10 currencies (even gaining slightly against USD). But assuming China growth holds up and oil prices slip, it could be the worst-performing of the three.

The oil industry seems to agree that oil is likely to fall next year, as supply increases faster than demand (see below). If that happens, I would expect CAD to decline somewhat. It’s been the best-performing of the three commodity currencies this year, indeed the best-performing of all the G10 currencies (even gaining slightly against USD). But assuming China growth holds up and oil prices slip, it could be the worst-performing of the three.

EUR/CHF is at its lowest level since June 2015, a few months after the Swiss National Bank (SNB) pulled the rug out from under the EUR/CHF floor (Jan 2015). What ever happened to the SNB Bank Council’s oft-repeated pledge that it “remains willing to intervene in the foreign exchange market as necessary, in order to counter upward pressure on the Swiss franc”?

EUR/CHF is at its lowest level since June 2015, a few months after the Swiss National Bank (SNB) pulled the rug out from under the EUR/CHF floor (Jan 2015). What ever happened to the SNB Bank Council’s oft-repeated pledge that it “remains willing to intervene in the foreign exchange market as necessary, in order to counter upward pressure on the Swiss franc”?

Perhaps they think it’s inevitable, given the way the Swiss economy has outperformed the Eurozone economy since the pandemic began.

Perhaps they think it’s inevitable, given the way the Swiss economy has outperformed the Eurozone economy since the pandemic began.

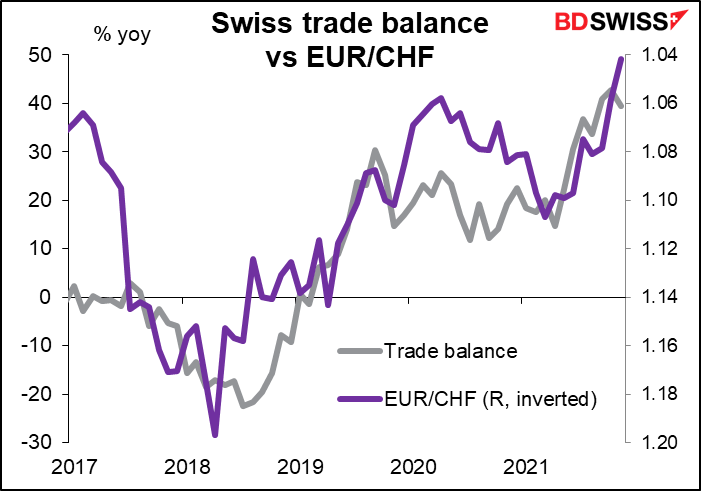

One reason the Swiss economy might be doing better than the Eurozone economy is that Swiss exports have held up well, causing a rise in the trade surplus.

One reason the Swiss economy might be doing better than the Eurozone economy is that Swiss exports have held up well, causing a rise in the trade surplus.

EUR/CHF has largely tracked the trade balance.

EUR/CHF has largely tracked the trade balance.

The yield advantage of CHF bonds vs German bunds (or more accurately the yield disadvantage of Bunds relative to CHF bonds, since both are negative) has narrowed considerably this year. That should’ve made it easier for the Swiss to recycle their trade surplus through portfolio investment.

The yield advantage of CHF bonds vs German bunds (or more accurately the yield disadvantage of Bunds relative to CHF bonds, since both are negative) has narrowed considerably this year. That should’ve made it easier for the Swiss to recycle their trade surplus through portfolio investment. However, portfolio investment abroad is just a small part of the recycling of the Swiss trade surplus. Direct investment is usually larger, but the Swiss have stopped direct investment abroad during the pandemic. Meanwhile, the central bank has pulled back from intervention (as mentioned above).

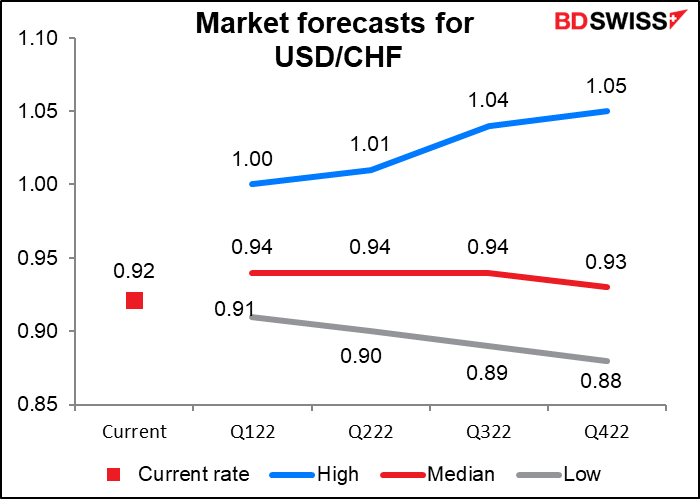

However, portfolio investment abroad is just a small part of the recycling of the Swiss trade surplus. Direct investment is usually larger, but the Swiss have stopped direct investment abroad during the pandemic. Meanwhile, the central bank has pulled back from intervention (as mentioned above). What’s to come? I agree with the market consensus of a higher EUR/CHF (weaker CHF vs EUR), mostly because I think Swiss companies will resume investing abroad. Furthermore, as interest rates around the world normalize, I would expect the “other investments” category – which includes loans – to move to an outflow as investors use CHF as a funding currency (along with JPY). Although CHF rates are expected to rise a tad faster than EUR rates (something I find difficult to imagine, but never mind), since they’re starting off 25 bps below EUR rates, they can rise a bit faster and still be below EUR rates. That makes CHF a good funding currency.

What’s to come? I agree with the market consensus of a higher EUR/CHF (weaker CHF vs EUR), mostly because I think Swiss companies will resume investing abroad. Furthermore, as interest rates around the world normalize, I would expect the “other investments” category – which includes loans – to move to an outflow as investors use CHF as a funding currency (along with JPY). Although CHF rates are expected to rise a tad faster than EUR rates (something I find difficult to imagine, but never mind), since they’re starting off 25 bps below EUR rates, they can rise a bit faster and still be below EUR rates. That makes CHF a good funding currency. Secondly, there’s a big question mark over Iran’s production, currently 2.52mn b/d or 9% of OPEC’s total output. If the Biden Administration works out some agreement with Iran – which looks increasingly unlikely – they could get the freedom to sell more oil. They have the capacity to pump 1.3mn b/d more so that would change the equation significantly. But if they don’t – which looks likely -- then their ability to maintain their oilfields will likely deteriorate, causing their output to fall. Ditto for Venezuela, also the object of a US trade embargo.

Secondly, there’s a big question mark over Iran’s production, currently 2.52mn b/d or 9% of OPEC’s total output. If the Biden Administration works out some agreement with Iran – which looks increasingly unlikely – they could get the freedom to sell more oil. They have the capacity to pump 1.3mn b/d more so that would change the equation significantly. But if they don’t – which looks likely -- then their ability to maintain their oilfields will likely deteriorate, causing their output to fall. Ditto for Venezuela, also the object of a US trade embargo. I think in the second half of the year, as economic activity gets back to normal (assuming economic activity gets back to normal!) oil prices could rise further.

I think in the second half of the year, as economic activity gets back to normal (assuming economic activity gets back to normal!) oil prices could rise further. The sad fact is, higher oil prices are needed to accomplish another goal of President Biden’s, that is, the switch to renewable energy. Nothing encourages investment in windmills and solar panels quite like $100/bbl oil. Not to mention that higher oil prices will be necessary to offset the risks involved in undertaking further exploration and development of long-term oil projects against the background of increasing pressure from the ESG movement (Environmental, Social and Corporate Governance) to move away from fossil fuels. Otherwise, there’s a risk of a serious debilitating spike in prices at some point in the decades before the transition to renewable energy is complete. As they say in the oil business, “high prices cure high prices.”

The sad fact is, higher oil prices are needed to accomplish another goal of President Biden’s, that is, the switch to renewable energy. Nothing encourages investment in windmills and solar panels quite like $100/bbl oil. Not to mention that higher oil prices will be necessary to offset the risks involved in undertaking further exploration and development of long-term oil projects against the background of increasing pressure from the ESG movement (Environmental, Social and Corporate Governance) to move away from fossil fuels. Otherwise, there’s a risk of a serious debilitating spike in prices at some point in the decades before the transition to renewable energy is complete. As they say in the oil business, “high prices cure high prices.” That’s certainly not impossible, but is it likely? In fact, the volatility of currencies has been falling for the last several years. It popped back up because of the pandemic but has since fallen back. It is entirely possible that we get a year of below-median volatility. But then again, we didn’t expect to get a global pandemic in 2020, did we?

That’s certainly not impossible, but is it likely? In fact, the volatility of currencies has been falling for the last several years. It popped back up because of the pandemic but has since fallen back. It is entirely possible that we get a year of below-median volatility. But then again, we didn’t expect to get a global pandemic in 2020, did we?

Not an existing member? Register an account in a few seconds, and gain unlimited access to exclusive research resources.

Access Leading Analysis, Market Briefs & Reports, Daily Live Webinars and much more!